Understanding Tax Payments under Self-Assessment: A Comprehensive Guide

Tax obligations can be a maze for individuals, and navigating through payment deadlines and requirements can be challenging. In this blog post, we’ll delve into the intricacies of payments under self-assessment, providing clarity on key dates, payment categories, and crucial details you need to know.

Payment Deadlines

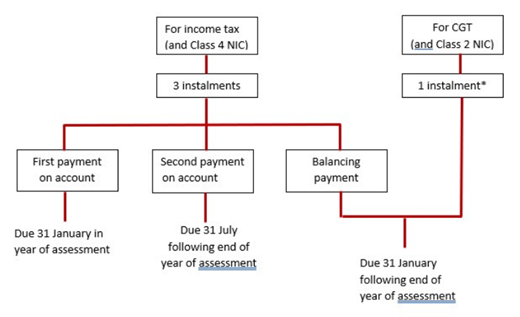

The primary deadline for individuals under self-assessment is January 31, following the end of the tax year. For the tax year 2022/23, this means payments are due by January 31, 2024. This encompasses various liabilities, including income tax, class 2 and class 4 national insurance, and capital gains.

Payments on Account

For some taxpayers, the process includes making payments on account for income tax and class 4 national insurance. This involves three instalments:

- First Payment on Account (Due: January 31, 2023): This aligns with the tax year, starting the process early.

- Second Payment on Account (Due: July 31, 2023): Providing an interim payment to spread the financial burden.

- Balancing Payment (Due: January 31, 2024): Ensuring that all obligations for the tax year 2022/23 are settled.

For residential property disposals, an additional payment on account must be made within 60 days of completion, adding another layer of consideration.

Income Tax Repayments

Repayments of tax under self-assessment typically follow the submission of the tax return. Timely submission, especially for paper returns by October 31, allows taxpayers to request HMRC to calculate their tax liabilities. Electronic returns automatically receive an online calculation.

Understanding Payments on Account

Payments on account are generally half of the income tax (plus class 4 NIC) due by self-assessment for the previous tax year. However, exceptions exist:

- No payments on account are required if:

- The income tax payable + class 4 NIC liability for the preceding year is less than £1,000.

- More than 80% of the income tax payable + class 4 NIC liability for the preceding year was settled via PAYE.

- First-year self-assessment: Only the balancing payment is due on January 31 following the tax year.

- Reducing payments on account: If the tax payable for the current year is expected to be less than the preceding year, payments on account can be reduced. Caution is advised to avoid excessive reduction, leading to interest on underpayment. Claims for adjustment must be made before payment deadlines.

Contact Us for Further Assistance

Understanding tax payments under self-assessment is crucial for financial planning. If you have questions or need personalised guidance, feel free to reach out to us at TaxDigit. Our team of experts is here to provide the support and information you need to navigate the complexities of tax obligations.

For further information or assistance, please contact us at +442035764595.

Remember, informed financial decisions start with understanding your tax responsibilities. Stay informed, stay compliant!